Simple Model for Building Wealth Part 2

Setting Wealth Goals

Start with Dreams

The purpose of wealth building goals is to set financial goals that, when reached, will support your dreams. We envision and describe the dream, and then we estimate the wealth needed. It’s not a perfect process, but here is an exercise to get you started.

Describe Your Perfect Day

Write a narrative description of what you have and what you do on a perfect day in your life when you have reached your goals. Be as descriptive as possible. Where do you live? What kind of car do you have? Who are the people around you? What activities are you doing? What is your health like? Where do you go? What interests are you fulfilling? Write as much as you can with as much detail as you can.

When you finished (at least for now), then make notes of what the values of the things are and the costs of services are. Of course, this is not exact. Think of the prices in today’s dollars. That is, if you had these things right now, then what would it all cost?

Some speed bumps in turning visions into goals

Some things are too dreamy or uncertain

For some of us, it’s hard to let your imagination go free if you’re not sure it’s possible, but just do your best. For things that are really dreamy, and you don’t know the costs, you might consider possibilities, like renting or leasing instead of buying. You don’t have to own everything in your dream.

Future costs might be completely different from current costs

True. There is no way to know with accuracy what your future cost budget will be. We will make adjustments for estimated inflation. We’re trying to get a direction and rough estimate.

My goal would be bigger if I knew what was possible

As you continue your quest, you will undoubtedly create more of your dreams in ways you cannot imagine right now. Think of all the things that we have in our lives today that didn’t even exist 20 years ago. What is possible continues to evolve.

For now, we are not going to constrain the dreams with strategies because we’re not going to constrain ourselves to the strategies we already know. What becomes possible for you may be much better than you know right now. You can’t see past the horizon. We keep moving forward and evolve dreams, goals, and strategies along the way.

Now make the cost of your dream a little more concrete

We’re putting an income number on your dream. You can revise it later and perhaps many times over your quest. We’re just setting direction right now.

Turn your cost estimates into a monthly income amount

I understand that’s another leap. But this kind of goal is one we can use for planning. Keep imagining and revising until you feel like the monthly income amount makes some sense to you. We don’t know how you’re going to get to the goal just yet - just that the goal is in the ballpark for being able to pay monthly expenses of your dream if you had the dream today. If you’re not sure, add some more income for a buffer. Or remove some of the really uncertain items just for now. You can adjust goals later.

Estimate the assets need that will pay the income you need

Initially, we will use a simple calculation to estimate the assets (investment amount) needed to generate the income to pay your estimated expenses. We working from today’s costs and today’s dollars for the moment.

Let’s say your estimated expenses are $10,000 per month. We will assume that we can generate 8% income from whatever assets we have accumulated.

12 months of $10,000 per month is $120,000 annual income required.

We assume 8% consistent income from our investments - that’s somewhat modest, but this is just the starting point

The required investment amount if we have the dream today is $120,000 / 8% = $1,500,000 or $1.5 million.

For many of us this amount gives us a queasy feeling. How in the world am I going to save that much money? What in the world am I going to invest in to get there? It’s going to take 30-40-50 years! Or I might never get there, and then I might run out of money because I never got to my goal.

Often this step is where we stop because the required investment level is already much higher (worse?) than we think is possible.

Unfortunately, the queasiness is going to get worse before it gets better

Every year that you have not yet reached your goal, the goal has to be increased by the amount of inflation. The math is easy, but it’s not simple to know what inflation really is. There are good reasons not to rely on the numbers given by governments and the Federal Reserve. There are also good reasons not to rely on the doomsayers that believe the dollar is going to crash next month.

I will help you with references about inflation (collecting them now). Eventually, you will just have to pick a number you believe enough in. You might have to adjust it from time to time. Keep in mind that eventually, you will have some investments and strategies that benefit from inflation, so you can have more peace of mind.

Revise your asset goal for each year you have not reached your goal

How can you say when you will reach your goal when you don’t know what’s possible? You don’t know what capital you’re going to have (or it seems like not enough), and the baseline rate (8%) is not enough to get there fast enough.

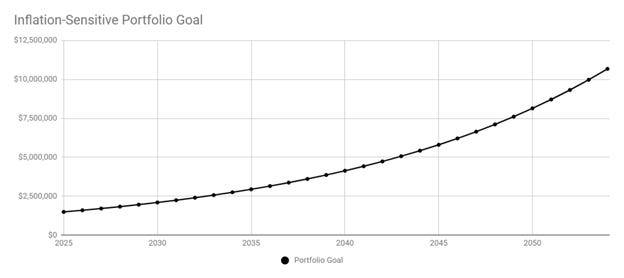

I get it. We’re not working on strategies yet, so we don’t know the time period yet. We’re still just setting the goal, and that goal moves each year. So we express the goal as a graph, like the one below:

This chart represents the goal that would preserve your purchasing power in an environment of 7% annual inflation with the intent of producing $10,000 per month income measured in today’s dollars with a portfolio yielding 8% per year.

The point at year 2025 is $1.5 million, just like we calculated. The required value of the portfolio in future years rises because of anticipated inflation of 7% per year. This graph shows the target portfolio value growing over 30 years.

The aha is that to reach our goal at any point in the next 30 years, we have to accumulate assets to or above this line. If, at any point in time, we have less than the assets on this line in the same year, then to reach our goal, we need to grow the portfolio faster than this line is growing. A few other ways to reach the goal could be

Reduce our income goal

Increase the income we get from the assets

Reduce our personal inflation rate by changing what we buy along the way or in retirement.

What’s next in the Simple Model for Wealth Building series

In the next piece, I will discuss factors that affect your portfolio goal: withdrawal strategy, handling inflation after retirement, safety, and taxes.

Disclaimer: This content is for educational purposes only. You should not construe any information or other material contained here or on our Sites at www.savvywealthtools.com or savvywealthtools.substack.com, as legal, tax, investment, financial, or any other professional advice. Nothing contained here or on our Sites constitutes a solicitation, recommendation, endorsement, or offer, by Savvy Wealth Tools or its owners, affiliates, or third party service providers to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.